ST. LOUIS ― Eighth District agricultural bankers reported that farm income had declined and that farm household spending and capital expenditures remained below levels compared with a year ago, according to the latest Agricultural Finance Monitor published by the Federal Reserve Bank of St. Louis. The number of bankers reporting third quarter declines was larger than 3 months ago and they expect farm income and expenditures to decline again in the fourth quarter.

The survey was conducted from Sept. 15, 2018, through Sept. 30, 2018. The results are based on the responses from 24 agricultural banks within the boundaries of the 8th Federal Reserve District. It includes all or parts of seven Midwest and Mid-South states: Arkansas, Illinois, Indiana, Kentucky, Mississippi, Missouri and Tennessee.

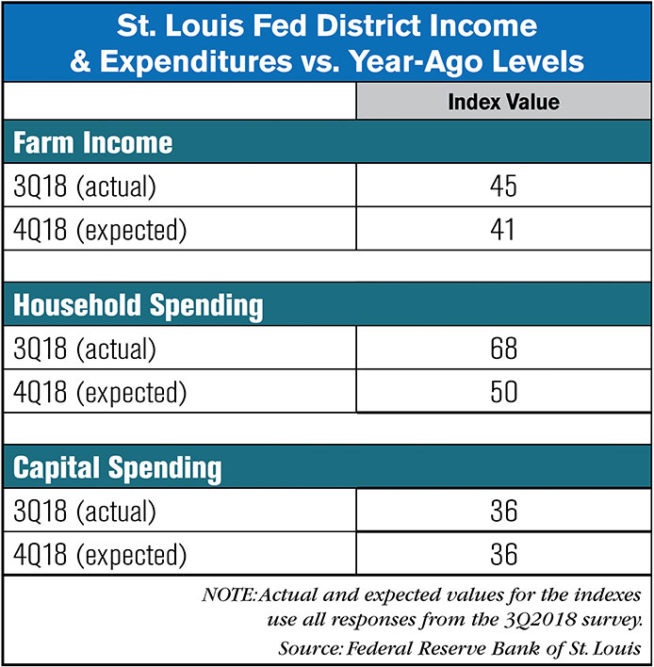

Farm Income Continues to Decline

The majority of agricultural bankers continue to report declines in farm income relative to a year earlier. The current index value marks the 19th consecutive quarter with a value below 100. Based on a diffusion index methodology with a base of 100 (results above 100 indicate proportionately more bankers report higher income compared with the same quarter a year ago; results lower than 100 indicate proportionately more bankers report lower income from a year earlier), the third quarter index value for farm income was 45.

Overall, bankers were slightly less optimistic when asked about the prospects for farm income in the fourth quarter of 2018. As one Missouri lender stated, farmers are hurting, “I expect no change in the marketing plans because they have bills to pay and will need to sell the crop to make those payments. Small farmers are hurting because of the low prices and are usually the ones who do not have on-farm storage to allow them to hold their harvested crops.” Bankers also reported that household spending and capital expenditures in the third quarter were lower than a year earlier.

Quality Farmland Values & Cash Rents Rose

Quality farmland values rose 2.5% in the third quarter along with ranchland or pastureland values which also increased by 1.5%. Cash rents for quality farmland rose 2% in the third quarter, while cash rents for ranchland or pastureland rose 0.8%. Bankers are split on whether cash rents for ranchland and pastureland will decrease or increase over the next 3 months.

Special Questions Regarding Development Concerns, Loan Repayments & U.S. Soybean Prices

The first special question revealed the top concern for bankers continued to be low commodity prices, as reported by a 77.3% majority. The second special question asked agricultural bankers which types of loans they expect to experience repayment problems over the second half of 2018. Nearly 71.4% of bankers expect the largest increase in repayment problems to be operating lines of credit.

U.S. soybean prices have fallen sharply since the Chinese government imposed tariffs on imports of U.S. soybeans in late July. This development caused some industry analysts to speculate that U.S. soybean producers would delay the marketing of all or part of their crop in the hope of a rebound in prices. A little more than half, 54.5%, responded to the third special question that soybean producers in their area do plan to delay selling all or part of their crop.

![[Technology Corner] Pessl Instruments CEO Talks Dealer Benefits From Lindsay Corp. Investment](https://www.agequipmentintelligence.com/ext/resources/2024/04/25/Pessl-Instruments-CEO-Talks-Dealer-Benefits-From-Lindsay-Corp.-Investment.png?height=290&t=1714144307&width=400)

Post a comment

Report Abusive Comment