By David B. Oppedahl, senior business economist

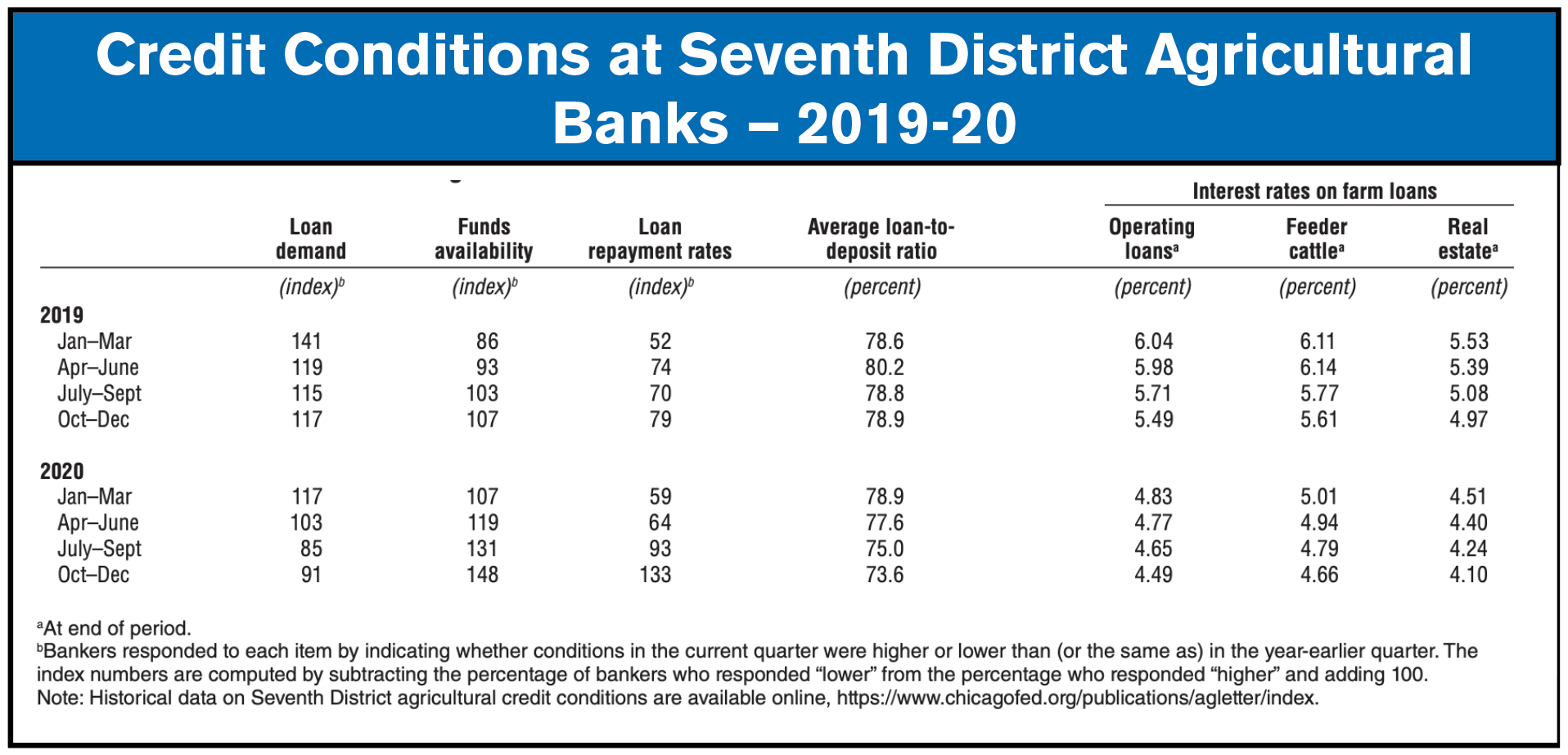

District agricultural credit conditions dramatically improved in the fourth quarter of 2020. The share of the District farm loan portfolio deemed to have “major” or “severe” repayment problems was 4.3% in the fourth quarter of 2020 — lower than the share reported in any final quarter since that of 2014. With 38% of survey respondents reporting higher rates of loan repayment and 5% reporting lower rates, overall repayment rates for non-real estate farm loans in the fourth quarter of 2020 were higher than in the same period of the previous year, which had not happened since the third quarter of 2013. At 133 for the final quarter of 2020, the index of non-real-estate farm loan repayment rates was last higher in the first quarter of 2013. Furthermore, non-real-estate farm loan renewals and extensions in the fourth quarter of 2020 were lower than in the fourth quarter of 2019, as only 7% of survey respondents reported more of them and 22% reported fewer.

As of January 1, 2021, the average interest rates for farm operating loans (4.49%), feeder cattle loans (4.66%), and agricultural real estate loans (4.1%) were at their lowest levels in the history of the survey. While interest rates moved down, the vast majority of banks did not change their credit standards for farm loans. Nineteen percent of the survey respondents reported their banks tightened credit standards for agricultural loans in the fourth quarter of 2020 from a year ago, while 2% reported their banks eased them. Similarly, 6% of responding bankers noted their banks required larger amounts of collateral for customers to qualify for non-real-estate farm loans during the final quarter of 2020 relative to a year ago, while 1% noted their banks required smaller amounts.

Demand for non-real-estate farm borrowing was lower during the October through December period of 2020 relative to the same period of 2019. With 17% of survey respondents reporting an increase in the demand for non-real estate farm loans from a year ago and 26% reporting a decrease, the index of loan demand was 91 in the fourth quarter of 2020 (close to its value of 85 in the third quarter). Funds availability was above the level of a year ago for the sixth quarter in a row. In the final quarter of 2020, the index of funds availability moved up to 148 (its highest value since the first quarter of 2013), with funds availability higher than a year ago at 49% of the survey respondents’ banks and lower at 1%. Moreover, the District’s average loan-to-deposit ratio kept slipping from its peak in the second quarter of 2019; at 73.6% for the fourth quarter of 2020, this ratio was 9.3 percentage points below the average level desired by the responding bankers.

Looking Forward

Survey respondents indicated that at the beginning of 2021, only 1.4% of their farm customers with operating credit in the year just past were not likely to qualify for new operating credit in the year ahead — this was an improvement from the percentage reported at the start of 2020. Farm real estate and non-real-estate loan volumes were projected to be larger in the first 3 months of 2021 compared with the same 3 months of a year ago.

Yet the mix of agricultural loan types was expected to change: Farm machinery and grain storage construction loan volumes were anticipated to increase, while the volume for operating loans was anticipated to be flat. At the start of 2021, survey respondents who forecasted capital expenditures by farmers would be higher in the year ahead compared with the year just ended outnumbered survey respondents who forecasted lower capital expenditures, reversing a trend of the past few years. An Illinois banker stated, “With the surge in commodity prices, I expect increased farmer spending on equipment upgrades.”

In addition, responding bankers anticipated higher expenditures by farmers for land purchases and improvements, as well as for buildings and facilities. For the first time since the first quarter of 2011, a majority of responding bankers (58%) predicted farmland values to go up in the next quarter (in this case, the first quarter of 2021). Notably, none of the survey respondents predicted farmland values to go down. The rest of the respondents (42%) predicted them to be stable. According to the survey results, the agricultural outlook seemed to be the rosiest in years.

![[Technology Corner] What an OEM Partnership Means to an Autonomy Startup](https://www.agequipmentintelligence.com/ext/resources/2024/09/26/What-an-OEM-Partnership-Means-to-an-Autonomy-Startup.png?height=290&t=1727457531&width=400)

Post a comment

Report Abusive Comment