North American farm equipment dealers are still cautious when it comes to projecting sales growth for all of 2017. At the same time, some dealers are seeing signs that sales trends are improving.

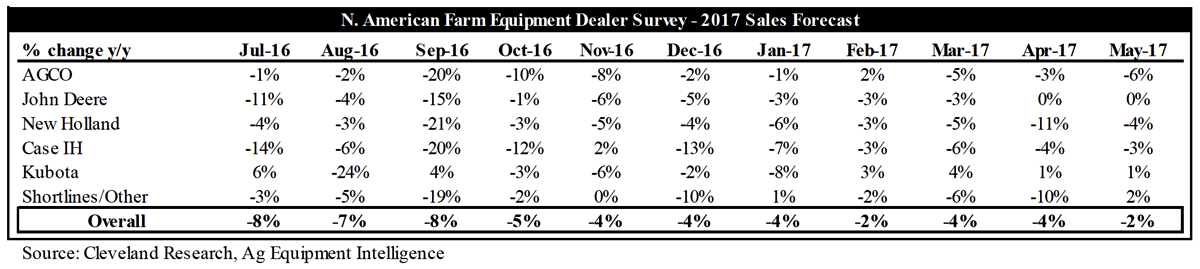

The 2017 sales growth forecast was reported at down 2%, an improvement from the year-to-date average of down 3% and down 4% in April. Commentary suggests weather and low commodity prices remain headwinds in the near term, but dealers remain optimistic on customer activity in the second half of 2017.

Dealer comments from the most recent Dealer Sentiments & Business Conditions Update survey included:

-

“We continue to be very optimistic about sales growth in 2017. The market is steady and the overall ag economy in our area is healthy. The used export market is especially strong for us and has contributed to increased new equipment sales.”

-

“Customers are interested in pre-sale planters for next year even with high new equipment prices and soft used equipment values. We believe new product technology is attracting customers despite a soft economy.”

-

“We saw better than expected sales in large 4WD tractors, self-propelled sprayers and air seeders, but combine sales remain weak.”

Compared to July 2016, overall dealers are solidly more optimistic. Results from that survey showed that overall dealers were looking at an 8% decline vs. the current 2% drop. During the past 11 months, both Case IH and John Deere dealers’ outlooks have improved significantly. Last July, Deere dealers were projecting an 11% decline vs. a current flat outlook. During the same period, Case IH dealers were looking at a 14% drop off last July compared to a 3% expected decline currently.

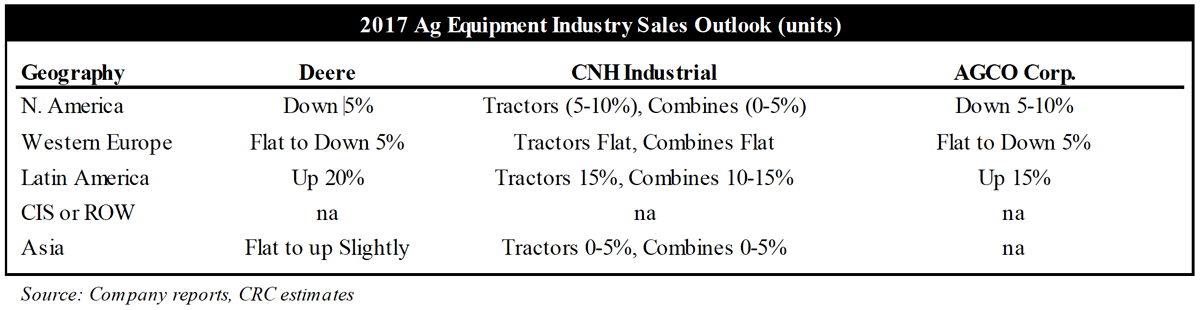

Based on their last earning reports, the major farm equipment manufacturers aren’t quite as confident in full-year 2017 results as their dealers. (See table below.)

Post a comment

Report Abusive Comment