Illinois farmland values continue at stable levels according to a March 19 report issued by the Illinois Society of Professional Farm Managers and Rural Appraisers (ISPFMRA).

“Farmland remains a stable, safe investment in volatile times such as we’ve seen so recently,” said David Klein, vice president with First Mid Ag Services, located in Bloomington, Ill. Klein serves as chair of the 2020 Illinois Farmland Values Survey and Conference. “Our survey data show the farmland price trends in the state continues to exhibit a stable pattern with little deviation from a year ago,” he said.

“In our year-end survey we capture the sentiment of what appraisers and farmland real estate brokers believe they are seeing,” Klein continued. “Dr. Gary Schnitkey, at the University of Illinois, polled their observations and outlook in our annual survey the second week of February. ISPFMRA and RLI (Realtors Land Institute) members monitor the pulse of the Illinois farmland market every day and the information in our Report suggests is there is significant variation between certain local areas within each region of the Illinois farmland market right now. The general opinion of our membership’s survey showed characteristics of a market that remains stable.

“Crop planting challenges across the state left the most unplanted acres since the spring of 1974. Most farm incomes were protected by crop insurance proceeds and USDA market facilitation payments,” said Klein.

The general trend indicated a stable market at year-end for both high quality farmland and lease rental rates. The central belt of the state seems to have the most consistent position of a stable-to-slightly-higher farmland market. Characteristics of farm sales in the data set for 2019 were slightly smaller in size and higher in quality, as compared to 2018. Challenges exist especially in the northeastern part of the state and lower quality soils in Southern Illinois.

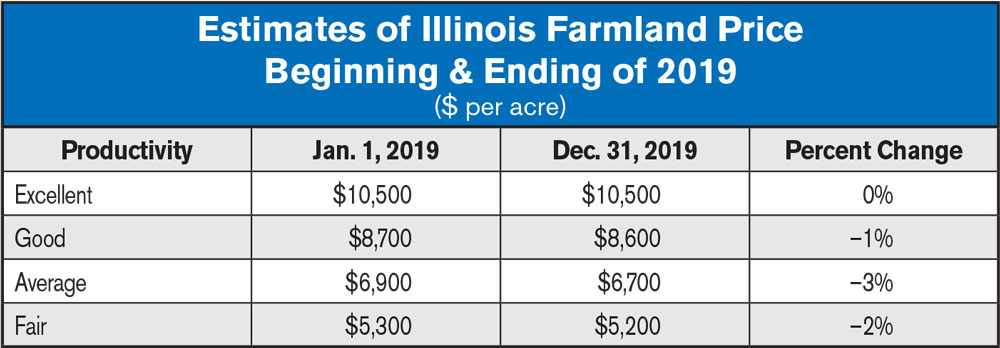

The overall summary of the complete survey is published in the 2020 Illinois Farmland Values and Lease Trends Report.

Dr. Bruce Sherrick, who compiled the land values data, and Dr. Gary Schnitkey summarized the results of the survey as follows:

• Sellers of Farmland — Settling estates was the number one reason for selling farmland, estimated as the reason for sale 58% of the time of Illinois farmland is sold. This is statistically the same for several years and an indication of a healthy farmland market. While Estate sales are estimated to be 44% of the volume of farmland sold in 2019, active farmer selling was estimated at 10%, which is 7% higher than the 3% estimated in 2012 when farmland values were nearing their peak. There may be a few more farmer-leaseback sales lately, than was experienced 5-plus years ago, an indication of higher cash needs in some farm operations.

• Buyers of Farmland — It is estimated farmers accounted for 59% of the purchase made in 2019. Most were reinvesting into their farm business — where they know the value as well as anyone. When farmers stepped aside, investors are looking for opportunities, especially in some of the more moderate land classes.

• Methods of Sale — More farms were sold by private treaty in 2019 than any other method, a continued trend from past years. This signals more negotiating was occurring as buyers attempt to minimize downside price risk. Some 33% of the transactions were estimated to be at auction, down from last year but about the same as 2018.

• Cash Rents — Generally speaking, farm incomes were slightly lower in 2019 as compared to 2018, with additional challenges anticipated in 2020. Frequently crop share leases turn over to at least a modified cash rent lease when land is bought and sold. Cash rents for 2019 were estimated $303 average rate on excellent quality farmland. Most ISPFMRA members expect 2020 cash rents on excellent quality soil farms to be near that same level. Landowners have been resistant to move much lower with the Market Facilitation Payments being received. Those payments helped with a short 2019 crop and moderate prices. In areas of Illinois with narrow cash grain basis, open market rental of farmland continues to be strong.

• Net Farm Income — Delayed spring planting or inability to plant carried trouble forward to farmer returns well beyond harvest. Government MFP Program payments provided many producers with a nominal amount of additional cashflow in the last quarter of 2019 or first quarter of 2020. Spring crop insurance prices will be lower for both corn and soybeans as compared to 2019. This, combined with the fact that most APH’s will be lower due 2019’s poorer yields, offers less overall revenue protection for 2020. On the expense side, real estate taxes continue to rise, and crop input providers are being challenged by farmers this winter to become more competitive to help their bottom line.

• Cash Return on Investment — The traditional 3.5-4.0% cash return on farmland investments is diminished by lower commodity prices and high input costs. Those net cash returns are now in the 2-3% range. Several investors still find this acceptable when looking at alternatives and the opportunity for portfolio diversification.

Macro-Economic Influencers

Interest Rates — Interest rates adjusted lower in 2019 and continue to be at historically low levels for borrowers. This is very supportive to farmland values from both a borrowing and alternative investment perspective. Lower interest rates force investors to look for alternatives to generate higher cash returns. Any return of rising interest rates was a concern to 68% of those surveyed.

Slowing Global Demand — 82% of survey respondents are concerned about further potential price decreases from lack of demand due to African Swine Fever, coronavirus scares and slowing global productivity, especially in China.

Government Policy — Optimistic talk of trade commitments with China and the USMCA agreement are seen as positive entering 2020. Market Loss Facilitation payments have helped “fill the gap” to help stabilize returns. The 2020 presidential election will be closely monitored for any changes in agricultural policy.

Growing Domestic supplies —With significant acreage increases for both corn and soybeans in 2020, 42% of respondents indicated they are concerned about falling commodity prices affecting land values if there are good U.S. growing conditions. Some 36% felt the same way about South America’s high production coming to market now.

Dollar Exchange Rate — Other worldwide currencies were devalued in the latter part of 2015 and early 2016 which made investment in anything American less attractive. Currency manipulation by certain countries and the U.S. Economy’s stability on a global scale has made the U.S. Dollar very strong, which is detrimental to export sales, and a key to higher U.S. grain prices. A strong dollar continues to be a head wind to American agriculture and land values. The high U.S. Dollar makes exportable ag products more expensive on the international market, as well as American land.

• Auction Sales —Auction sales continue to show pockets of strength and relative softness. Class A Farms selling in the $12,000’s per acre, late in 2019 and early 2020 show strength still exists in areas. However, it takes a tight supply and at least two motivated buyers to make a good auction. In some cases that is all that are present as the number of active bidders at each auction were diminishing prior to the financial markets being so volatile. It will be interesting to see if that changes with new perspectives and lower interest rates.

• Transitional/Development Land — Very few tracts of land continue to be sold for development. While new construction activity is slowly picking up in the “metro-east area of St. Louis” and collar counties of Chicago, many are in existing subdivision developments that were started 10-plus years ago. As a result, very little 1031 tax deferred exchange money exists in the current market. When those buyers were present, they definitely helped absorb supply.

• Institutional Money — Larger tracts of land continue to draw interest from institutional investors, pension funds, international buyers and others. This source of demand for farmland in Illinois has likely kept values more stable than restrictive ownership states west of the Mississippi River. Institutional buyers will often look to purchase tracts that will provide a higher cash return and absorb moderate quality farmland available in the marketplace. Illinois is friendly to this type of buyer and will be needed in 2020.

• Farmland Availability — Farmland supply to the market remained fairly tight throughout 2019. 71% believed there was either the same volume or less farmland available to purchase in 2019 as compared to a year ago, while 29% thought there was at least some increase in supply. This variation in opinion speaks to the volume of land available in certain markets.

Post a comment

Report Abusive Comment