After several difficult years, it looks as if U.S. and Canadian farm equipment dealers are back on firm footing. With that said, probably the best thing the industry can do moving forward is to not compare current conditions to the boom years of 2008-14, which were not typical, and acknowledge that the ag equipment business is actually returning to a more normal state.

Generally, sales of large and mid-size ag machinery saw a mild, but welcomed upturn in the past year, and small equipment sales maintained its strong, upward trend. Most dealers expect more of the same in 2019, according to their responses to Farm Equipment’s 2019 Dealer Business Outlook & Trends survey.

It’s a pretty good bet if the dealers’ forecast that the year ahead will be as good as or better than the past year overall, 2019 should be a profitable year for most farm equipment retailers.

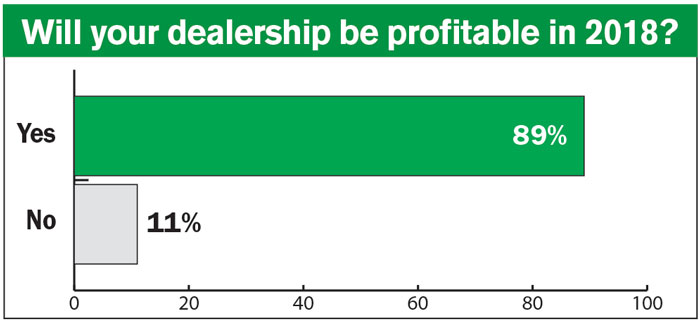

In the 2019 survey, a couple of additional questions were asked about dealers’ business performance in 2018. The first was, “Will your dealership be profitable in 2018?” Nearly 90% of the dealers participating in this year’s survey responded “yes.” The remaining 11% said “no.”

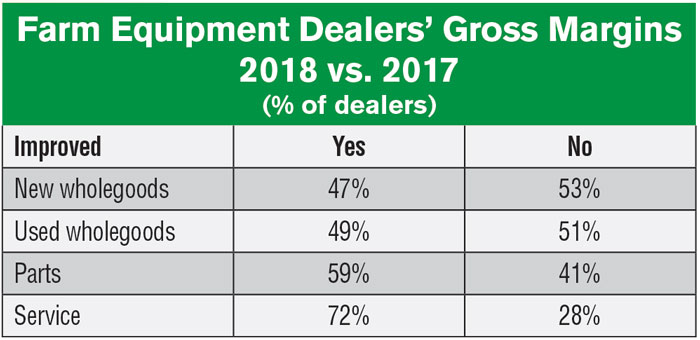

The second new question was, “Will your gross margins improve in 2018 vs. 2017?” Parts and service turned in a strong performance for the year, but gross margins on wholegoods sales, both new and used, didn’t fare as well.

Dealers’ Outlook for 2019

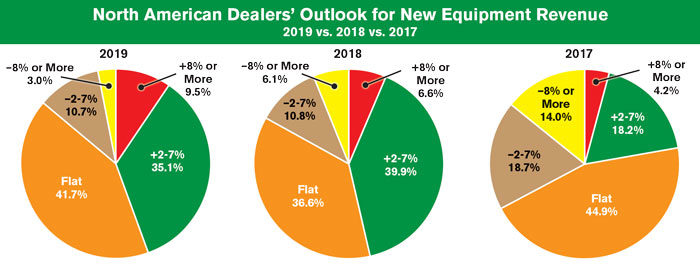

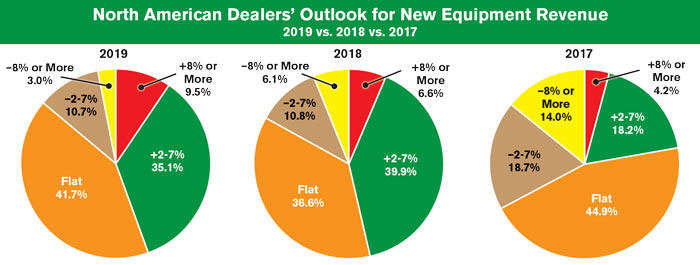

North American ag equipment dealers are generally optimistic about their prospects for improving new and used equipment revenues moving into 2019. In fact, their outlook for the new year is very similar to the sentiments they expressed a year ago when it comes to revenue gains. The only noticeable difference is 5% more dealers expect revenues to be flat in 2019 (42%) than did in 2018 (37%). At the same time, about 3% fewer dealers see new equipment revenues dropping off in the year ahead than projected declines last year.

Nearly 45% (44.6%) of North American farm equipment dealers expect revenues from the sale of new equipment to increase by 2% or more in 2019. This is down slightly from the previous year (46.5%) but still up significantly from 2017, when only 22.4% of dealer projected higher revenues.

New Equipment Revenues: Overall, 86% of dealers are projecting 2019 new equipment revenues will be as good as or better than 2017. A little less than 14% of dealers expect new equipment revenues to decrease in the new year. This is a small improvement compared to the 2018 survey when 83% of dealers anticipated increased revenues and 17% projected declining new equipment sales. But it’s a significant improvement over two years ago when 67% of dealers forecasted improving revenues of new machines and 33% projected declining sales.

A breakdown in the projections for 2019 show 9.5% of dealers anticipate increases of 8% or more and 35.1% say their revenue improvement will be in the 2-7% range. Of the 13.7% of dealers expecting a drop off in new equipment revenues, 10.7% are preparing for declines in the 2-7% range and about 3% expect a drop of 8% or more. The remaining 42% are forecasting flat revenues for the year.

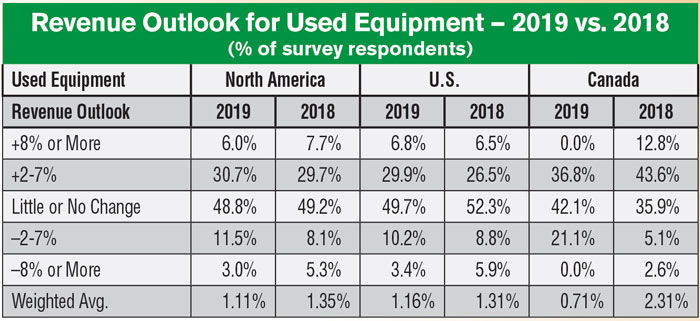

The percentage of dealers looking for an increase in revenues from the sale of used machinery fell slightly, from 37.4% a year ago to 36.7% for 2019. A slightly larger percentage are also projecting a decrease in revenues, with 14.5% expecting a decrease vs. 13.4% a year ago.

Used Equipment Revenues: On the used machinery side for 2019, the trend is identical on the plus-side to what dealers expect with new equipment sales. Nearly 86% see revenues from used sales being as good or better than the previous year, while a little over 14% are projecting a falloff in revenues. This projection also matches up well to expectations a year earlier when about 87% predicted used machinery sales revenue would improve and 13% saw them declining. Two years earlier, 24% of dealers forecasted falling revenues from used equipment sales.

Segmented further, the survey results indicate that 6% are calling for an increase of 8% or more in their used equipment revenues for 2019, while nearly 31% are calling for increases of 2-7%. Of the dealers expecting declining revenues from used sales, 11.5% see drops of 2-7% and 3% anticipate larger declines of 8% or more.

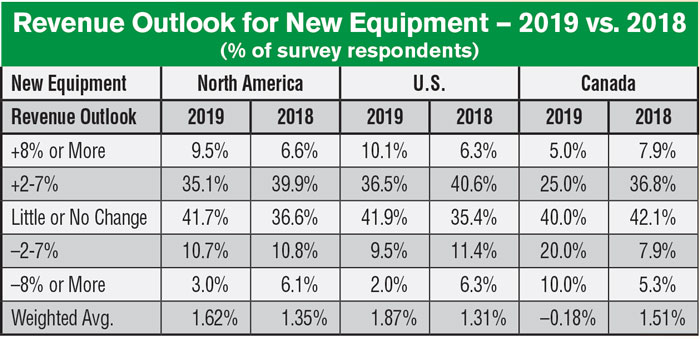

U.S. & Canada New: Generally, U.S. dealers are more optimistic about their potential to increase new equipment revenues in 2019 than are their Canadian colleagues. In terms of new equipment sales, more than 88% of U.S. dealers project that revenues will be as good or better than they were in 2018. This is about 6% higher than a year ago. Of these, 10% see sales improving by 8% or more, 36.5% expect growth in the 2-7% range and 42% are forecasting flat revenues for the new year. Only 11.5% expect a falloff in new equipment revenues. About 2% of dealers see revenues falling by 8% or more and 9.5% expect declines of 2-7%.

Meanwhile north of the border, 80% of Canadian dealers expect as good as or better than 2017 revenue levels in 2018 for new equipment. But in their case, only 5% are forecasting gains of 8% or more, 25% are calling for increases of 2-7% and 40% expect little or no change compared to 2017 levels.

U.S. & Canada Used: The outlook for revenue from the sale of used ag machinery is not quite as optimistic as it is for new equipment in either the U.S. or Canada, but it is similar for both countries. Overall, nearly 37% of dealers in both countries expect an increase in used equipment revenues in 2019.

More than 86% of U.S. dealers expect their sales of used machines to be as good as or better than what they saw in 2018. Of these, about 7% expect an increase of 8% or more, 30% look for a pick up of 2-7%, and nearly 50% anticipate little or no change in used revenues in 2019. Less than 14% are projecting a decline in sales of used equipment.

No Canadian dealers expect a significant increase of 8% or more in used machine sales in 2019, but 37% project gains of 2-7% and 79% anticipate little or no change. A little over 21% are planning for declining sales in this area of their business.

How Did North American Dealers Fare in 2018?

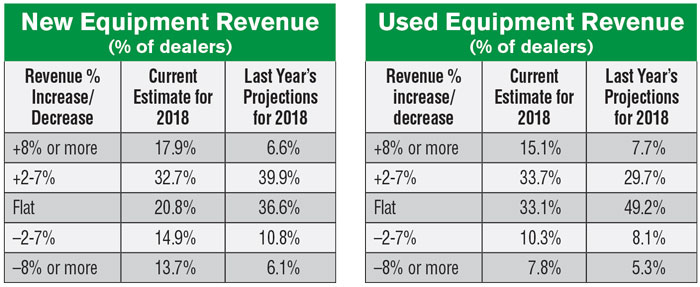

A year ago, North American farm equipment dealers were asked to estimate how they would finish 2018 in terms of increased or decreased revenue from new wholegoods sales vs. the previous year. At the time the 2018 Dealer Business Outlook & Trends survey was conducted in early September, nearly 47% estimated revenues would be up. Of this group of dealers, 6.6% projected revenues would be up 8% or more and nearly 40% projected increases of 2-7%.

As a follow-up, in this year’s survey dealers were asked where revenues from new wholegood sales would actually finish in 2018. A little over half (51%) said they would see an increase in new sales. Taken as a whole, the percentage of dealers expecting to see business conditions improve in the past year were not too far off, +4%, from the number who are reporting they’ll finish in the black when they close the books on 2018.

When it comes to the actual breakdown of the numbers, though, the dealers were farther off in their projections last year than what they’re reporting currently, 12 months later.

For example, nearly 37% of dealers last year were forecasting flat sales. Only 21% are reporting that sales were flat in 2018. Also, 6.6% of dealers last year expected new wholegoods revenue to grow by 8% or more.

As the final numbers are now in sight, 18% of dealers are reporting their new revenues grew by 8% or more. This was offset by 40% dealers who last year projected sales revenues would increase by 2-7%. The current survey shows that 33% of dealers saw increases in this range in the past year.

Unfortunately, more dealers (nearly 29%) are reporting they experienced a dropoff in new equipment revenue in 2018. Last year, only about 17% expected new wholegood revenues to decline.

Used Equipment in 2018: A year ago, 37.4% of ag machinery dealers anticipated increased revenues from used equipment sales. Currently, almost 49% says they’ll finish up 2018 in positive territory; 15.1% up 8% or more; 33.7% up 2-7%.

Nearly half of the dealers last year forecasted little or no change in used machinery sales. In the newest survey, only 33% report that used sales will be flat during 2018.

On the other hand, a year ago only 13.4% of dealers anticipated declining sales of used equipment for 2018. Slightly over 18% are reporting revenues for used sales dropped off during the year.

Early Order Levels Improve

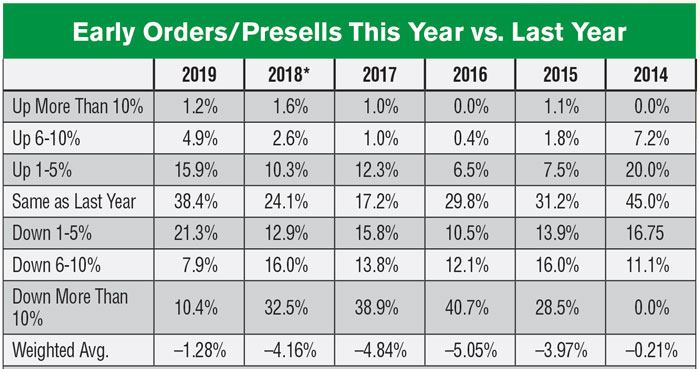

How farmers respond to early order discount programs is often considered a prime indicator or signal whether or not equipment sales would increase or decrease in the year ahead. If this bellwether holds true, 2019 could prove to be a better year than 2018.

According to the data from last year’s survey, only about 15% of dealers indicated that their early orders had improved vs. 5 years ago, while 61% reported their early orders were down year-over-year. Going into 2019, 22% of dealers are reporting higher pre-sells than they saw for 2018, and a little less than 40% of dealers say early orders declined from the previous year.

*The 2018 Outlook & Trends survey asked dealers to compare early orders/presells vs. 5 years ago, while the 2019 survey returned to the practice of asking for year-over-year comparisons.

On a weighted average basis, this is the most significant improvement observed in the past 6 years. While still in negative territory, the 2019 weighted average improved to –1.28% from –4.16% for 2018.

The percentage of dealers indicating higher pre-sells in 2019 increased in the +1-5% and +6-10% categories, which showed noted increases of 5.6% and 2.3%, respectively. Likewise, those who reported declining early orders decreased by 22% in the –10% or more category and by 8% in the –6-10% bracket.

For comparison purposes, 2 years ago in the 2017 survey nearly 69% of dealers reported their early orders were down and in 2016, 73% of dealers said their pre-sells had declined compared to the previous year.

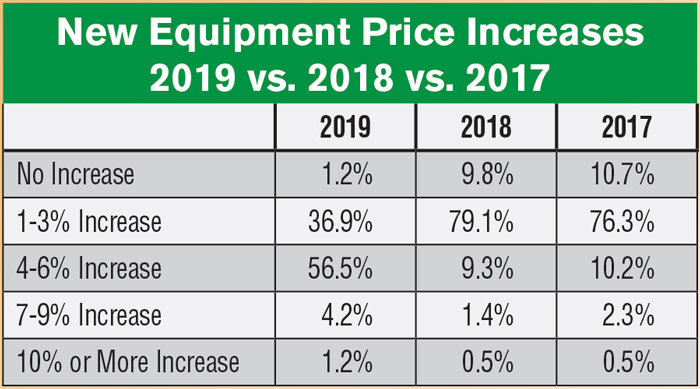

Along with the growing need for farmers to replace aging equipment, it has also been suggested that the increase in early orders was helped along by anticipated price increases. The tariffs on steel and aluminum implemented earlier in the year combined with typical increases from equipment manufacturers probably prompted farmers to take advantage of early order discounts.

Across the board, more dealers are expecting new equipment price increases for 2019, and it appears the price hikes will be of a larger magnitude than what’s been seen the past few years. Only 1.2% of dealers indicate they don’t expect any increases. This is down from 10% the previous year and 11% two years ago who didn’t expect higher prices for new equipment. The biggest percentage of dealers, 57%, anticipate increases in the 4-6% range in the year ahead.

Tractor & Combine Sales Gain Momentum

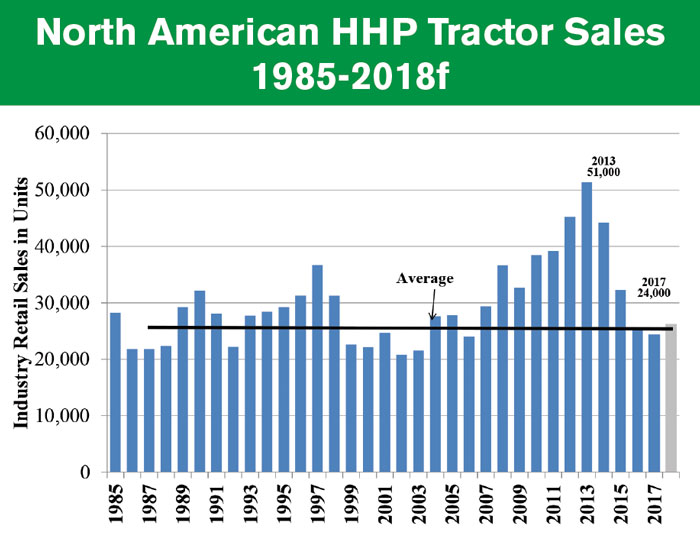

If North American sales of high horsepower and large 4WD tractors maintain their current momentum through the end of 2018, total turnover for the year will end up just about, or slightly higher than, the average annual unit sales since 1985 — or approximately 25,000 units. At the same time, they will still be only about one half of what we saw during the peak year of 2013 when sales of this equipment topped 51,000 units.

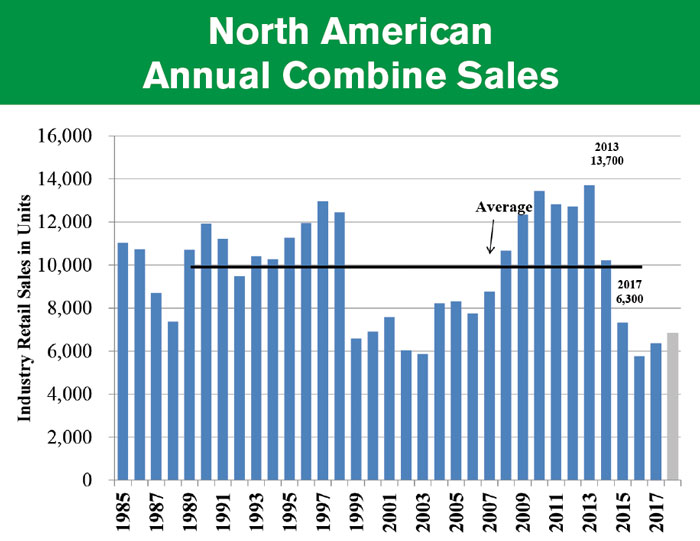

Meanwhile, North American combine sales are still looking to get back to an “average” year. Since 1985, the average annual sales of combines in the U.S. and Canada has been about 10,000 units. Last year, farmers purchased 6,300 combines. In the peak year of 2013, the industry moved about

13,700 units.

Through the first 8 months of 2018, North American sales of high horsepower and 4WD tractors are up 8.4% and combines are up nearly 14% compared to the same period of 2017, according to data released by the Assn. of Equipment Manufacturers.

Through the first 8 months of 2018, compact tractor sales (less than 40 horsepower) continued to set records. AEM reports that U.S. sales of the small equipment from January–August were up 10.5%. Canadian sales were also up year-over-year by 4.5%. Mid-range tractor sales in the U.S. (40-100 horsepower) were up 2.5% for the same period, while Canadian sales of utility equipment was only 0.2% higher.

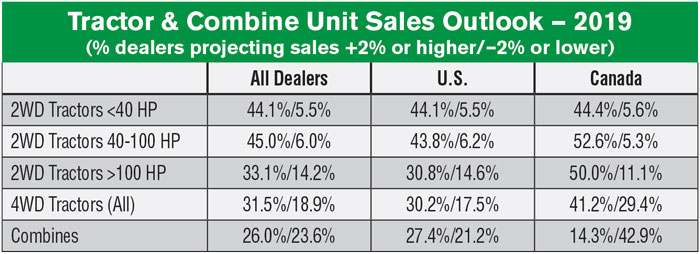

Tractor & Combine Outlook: Dealers’ view of tractor and combines sales for 2019 is mixed, but somewhat better than it was a year earlier. Once again, U.S. dealers are a tad more optimistic than their Canadian colleagues.

Starting with the bigger equipment, 33% of North American dealers forecast a pick up in sales of row-crop tractors (>100 HP), while 14.2% are expecting sales to decline. This is slightly better than the 31.6% who were looking for gains and 13.7% who anticipated a falloff in sales last year. There is little change in dealers’ outlook for improved sales of 4WD equipment in 2019 (+31.5%) and how they saw it a year ago (+31.3%). A major difference can be seen in the percentage of dealers looking for a drop in 4WD tractors in the year ahead. Last year, only 7.4% expected sales to decline vs. nearly 19% for 2019.

Following the sales boom years of 2008-14, the sale of high horsepower tractors (row-crop and 4WD) have tailed off and returned to more normal levels. Source: AEM, Cleveland Research Co.

Annual combine sales reached a peak in 2013 before seeing significant declines, but have been slowly increasing since 2016. Source: AEM, Cleveland Research Co.

Dealers see much better prospects for improving sales of utility tractors in the year ahead than was the case 12 months earlier. Some 45% of dealers are projecting improved sales of mid-range equipment in 2019 and only 6.0% are anticipating sales to decline. Last year, about 36% anticipated improving sales and 6.2% forecasted a sales slowdown.

Enthusiasm for increased sales of compact tractors in 2019 is a carryover from the year before. Looking ahead, 44% of dealers a projecting increased sales vs. 40% a year earlier. Only 5.5% are expecting sales to fall in the year ahead, while last year 7.3% of dealers predicted declining sales.

New Holland Dealers Most Optimistic for 2019

Breaking the survey responses down by brand shows New Holland dealers have the highest hopes for increasing new equipment revenues going into the new year. Overall, nearly 57% of New Holland dealers expect new machine sales to increase in 2019: 8.7% up 8% or more; 47.8% up by 2-7%.

AGCO dealers trailed the leaders by about 4%, with 53% projecting increasing new equipment sales in the year ahead: 20% up 8% or more; 33% up 2-7%. They were followed by Kubota dealers, 50% of whom forecasting a jump in sales revenues: 9% see an increase of 8% or more and 41% anticipating rising revenues in the 2-7% range.

They were followed by John Deere equipment dealers. With nearly 45% expecting improved revenues from new equipment, 8% projecting an increase of 8% or more and 37% who see growth of 2-7%. Deere dealers were only one of two groups who also expected revenue drops of 8% or more. Over 5% of dealers listing Deere as their major equipment supplier expect revenues to fall off by 8% or more. The other group was the independent, or shortline-only dealers. About 26% of this group projected increased new equipment revenues in 2019 (16% up 8% or more; 10% up 2-7%), but the same percentage (26%) expect sales to decline in the year ahead.

Nearly 43% of Case IH retailers see improving new equipment revenues in 2019. The 6% of these dealers who are forecasting increases of 8% or more was the smallest percentage of all the groups. The remaining 37% of Case IH dealers who anticipate improving revenues are calling for gains of 2-7%.

2019 ‘Best Bets’

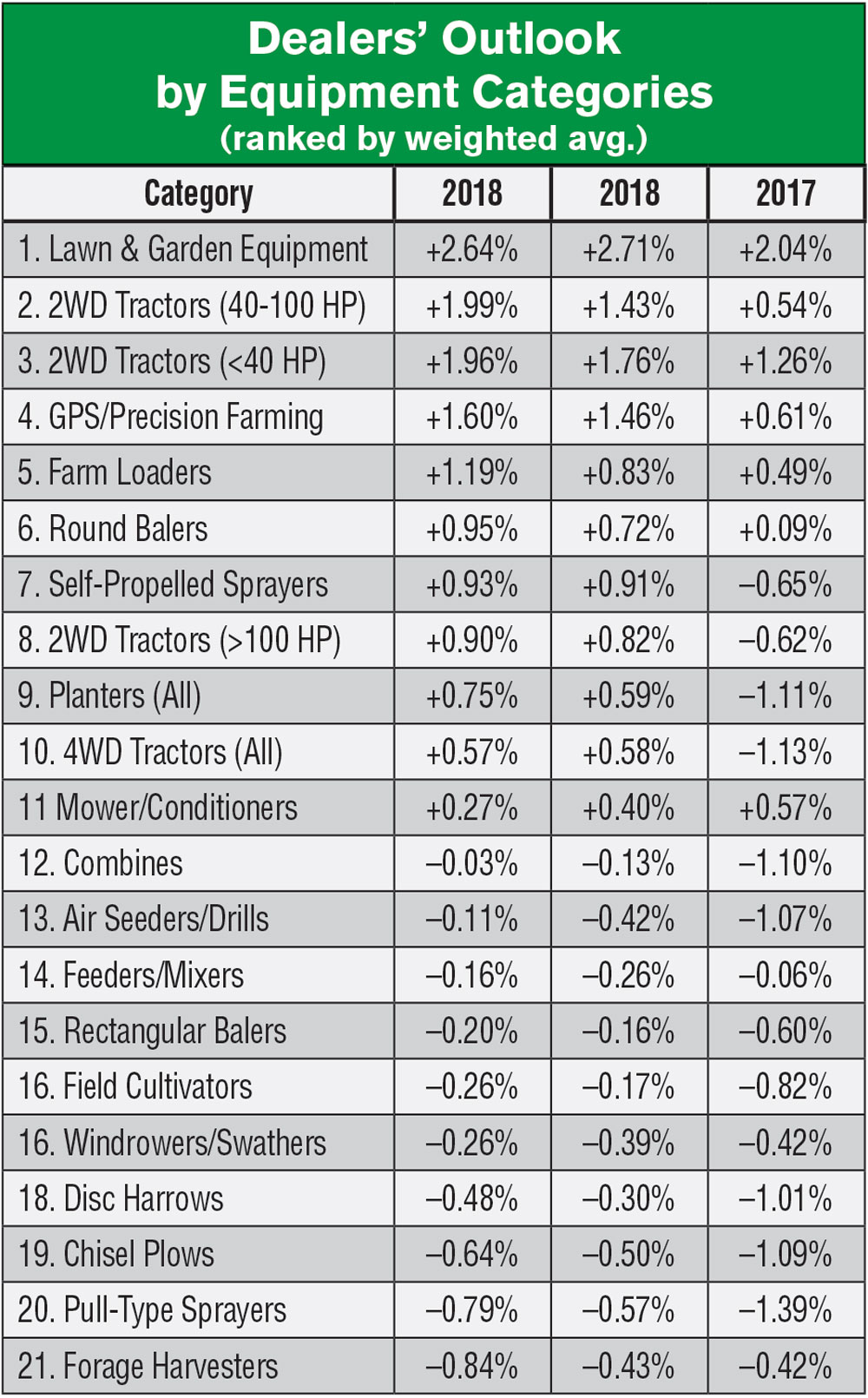

Dealers were also given a list of different equipment categories and asked to estimate the change they would see in unit sales of each in 2019 compared to the current year.

As it turns out, the lawn and garden category was again North American dealers’ “best bet” to bring in more money in 2019. Of the 21 equipment categories, the highest percentage of dealers (53.6%) forecasted lawn and garden equipment sales to increase by at least 2%. The category also received the highest weighted average of +2.64%, more than one-half a percentage point higher than the next-closest weighted average (+1.99%), which went to mid-size tractors.

Lawn and garden equipment is proving to be a reliable category year to year, judging by the last couple years of Outlook & Trends survey data. The highest percentage of dealers also picked the equipment category to see sales growth of 2% or more for the year 2018; the category also garnered the highest weighted average in at least the last three surveys.

Following that, the next “best bet” for dealers was midsize tractors. For this equipment category, 45% of survey respondents projected a sales increase of at least 2%. Following midsize tractors are: small tractors (44.1%), precision farming equipment (40.4%) and high horsepower tractors (33.1%).

Forage harvesters appear to be the least likely to generate more money in 2019, as only 4.2% of dealers indicate they expected sales that equipment category to increase by 2% or more. Forage harvesters’ ranking among all equipment categories fell to the bottom after being ranked 19th overall in terms of forecasted unit sales growth for 2018.

Following behind forage harvesters are: pull-type sprayers (5%), chisel plows, (7.4%), feeders/mixers (9.4%) and field cultivators (11.9%).

None of those equipment categories saw the highest percentage of dealers forecasting unit sales to decrease, however. That title goes to combines, for which 23.6% of dealers said they expect declining sales. At the same time, 26% of dealers also projected unit sales to increase for the equipment category, placing it in 11th in the “Best Bets” list, which ranks products based on the number of dealers who project unit sales to increase by 2% or more.

The feeders/mixers category saw the largest percentage of dealers who said there would be little to no change in unit sales in 2019 vs. 2018, at 80.3%. Following that category are forage harvesters and pull-type sprayers, both of which saw 78.2% of dealers projecting little or no change in sales.

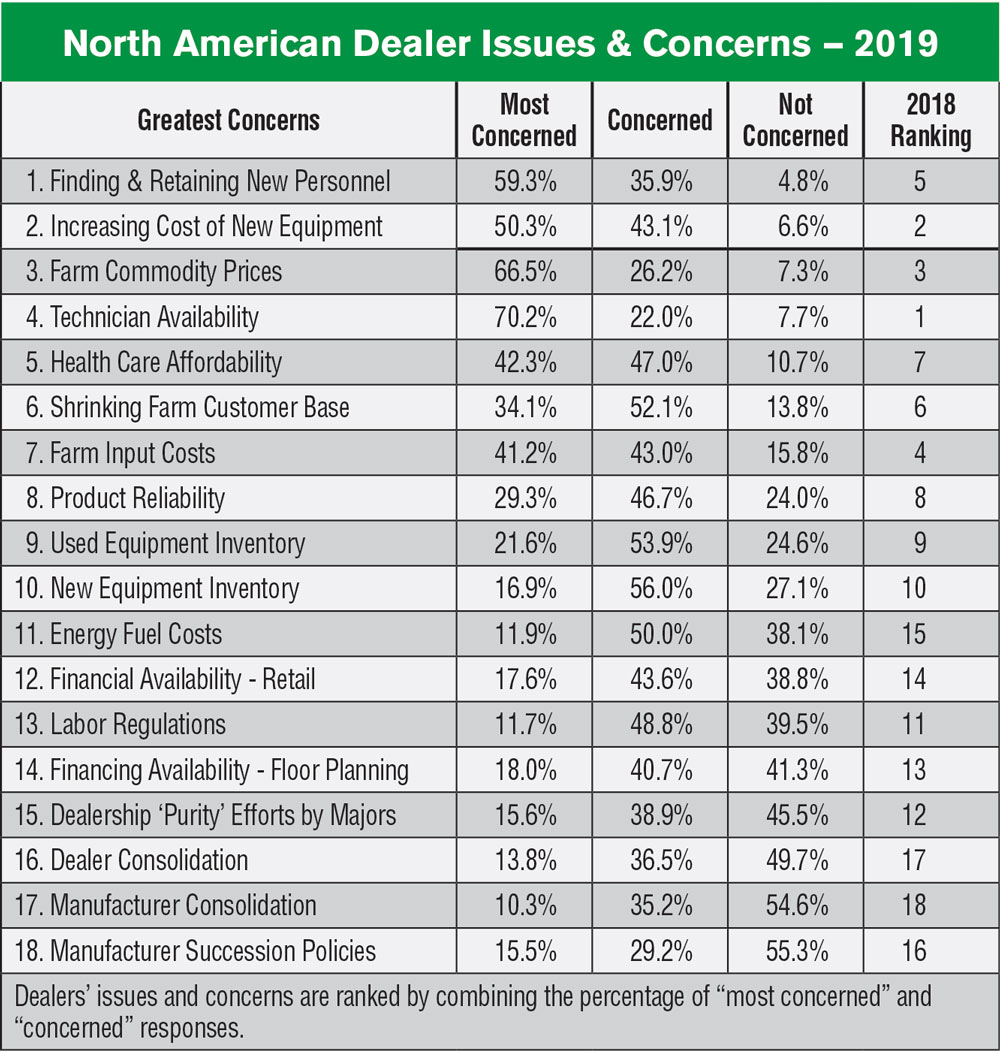

Finding Workers a Rapidly Growing Concern

As part of the survey, dealers are regularly asked about the issues they find most concerning for the coming year. Respondents are given a list of issues and are asked to indicate for each whether they are “not concerned,” “concerned” or “most concerned.”

Rising from the fifth most concerning issue to dealers in 2018, finding and retaining new personnel skyrocketed to the top concern of dealers headed into 2019. Dealer concerns are ranked by combining the percentage of those who indicated “most concerned” and “concerned” in their survey responses. Specifically, 95.2% of dealers indicated they are either “most concerned” or “concerned” with hiring and retaining employees in 2019.

Dealers are also concerned about technician availability, with 92.2% saying they are either “very concerned” or “concerned” about the issue. Technician availability is down from the top dealer concern in 2018 to the fourth-biggest concern in 2019.

It is no coincidence that two of dealers’ top five concerns for the coming year are related to the number people they have on staff. The national unemployment rate was below 4% as of August and is even lower in some states. Outside of this year, there have not been this few people without jobs who are actively looking since December 2000, according to the U.S. Bureau of Labor Statistics. Many industries are suffering from significant shortages of skilled workers.

Rounding out the top five most concerning issues for dealers is the increasing cost of new equipment (with 93.4% of dealers indicating “concerned” or “most concerned”), farm commodity prices (92.7%) and health care affordability (89.3%).

Dealers indicated they are least concerned about manufacturer succession policies (44.7% are either “most concerned” or “concerned”), followed by manufacturer consolidation (45.5%) and dealer consolidation (50.3%).

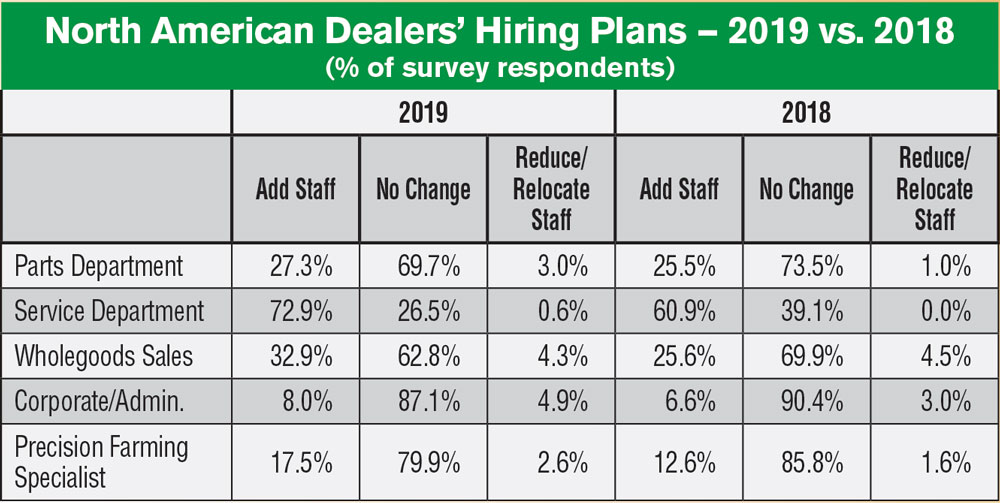

Dealers Planning to Grow Service Department Staff

Dealers may be worried about finding enough people, but this doesn’t necessarily mean they have big plans to add staff to their payrolls — at least not in every department. A majority of dealers said they were planning to add employees in only one area: the service department. Nearly 73% of survey respondents said they planned to add staff to that department in 2019, up from nearly 61% in 2018.

Even so, more dealers are indicating they plan to add staff in each area of their business on a year-over-year basis. For instance, 27.3% of dealers say they will add parts department staff in 2019 vs. 25.5% who said the same thing the previous year, while 32.9% of dealers plan to expand wholegoods sales staff for 2019 vs. 25.6% in 2018.

More than 87% of dealers indicated they don’t plan to add or reduce corporate and administrative staff in 2019, making this department the least likely to see any change in headcount for the coming year.

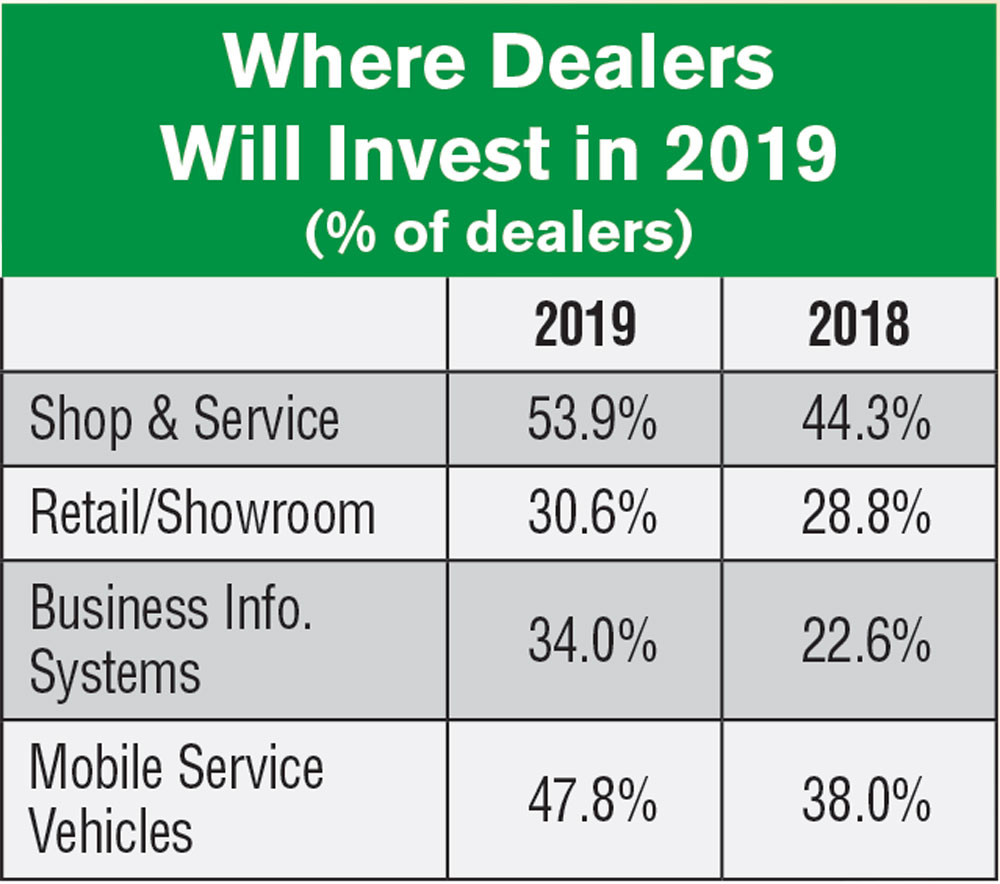

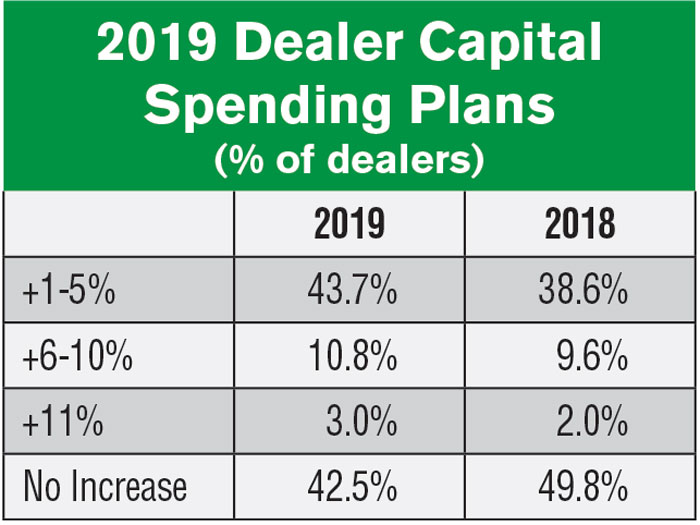

Capital Spending on the Rise for Most Dealers

More than half (57.5%) of dealers say they will increase capital spending by at least 1% next year, an increase from the 50.2% who said they planned to increase capital spending in 2018. Of those dealers who will be spending more in 2019, most (43.7% of all respondents) are projecting increases of 1-5%, compared with 38.6% who said they would increase spending in that range for 2018.

A majority of dealers (53.9%) plan to increase capital expenditures for shop and service improvement projects. This is up from 44.3% in 2018. Nearly half (47.8%) said they would increase capital spending for mobile service vehicles, a significant jump from the 38% who indicated the same last year. Capital spending related to showroom improvements as well as business information systems (computer hardware and software) are also on the increase relative to 2018.

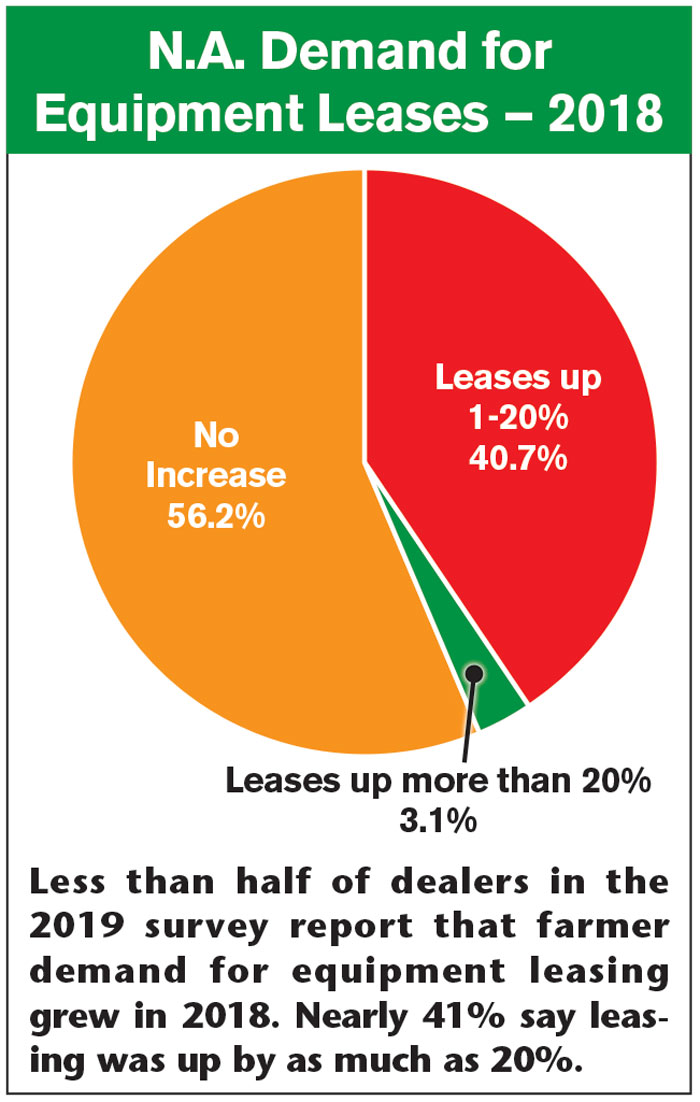

Lease Demand Down in 2018

Most dealers responding to the Outlook & Trends survey indicated farmer demand for equipment leasing either stayed steady or decrease in 2018. More than 56% of dealers said customers’ demand for equipment leasing did not increase in the past year vs. the previous year, while 40.7% indicated lease demand was up between 1-20%.

USDA Expects 2018 Farm Profits to Dip to 2016 Levels

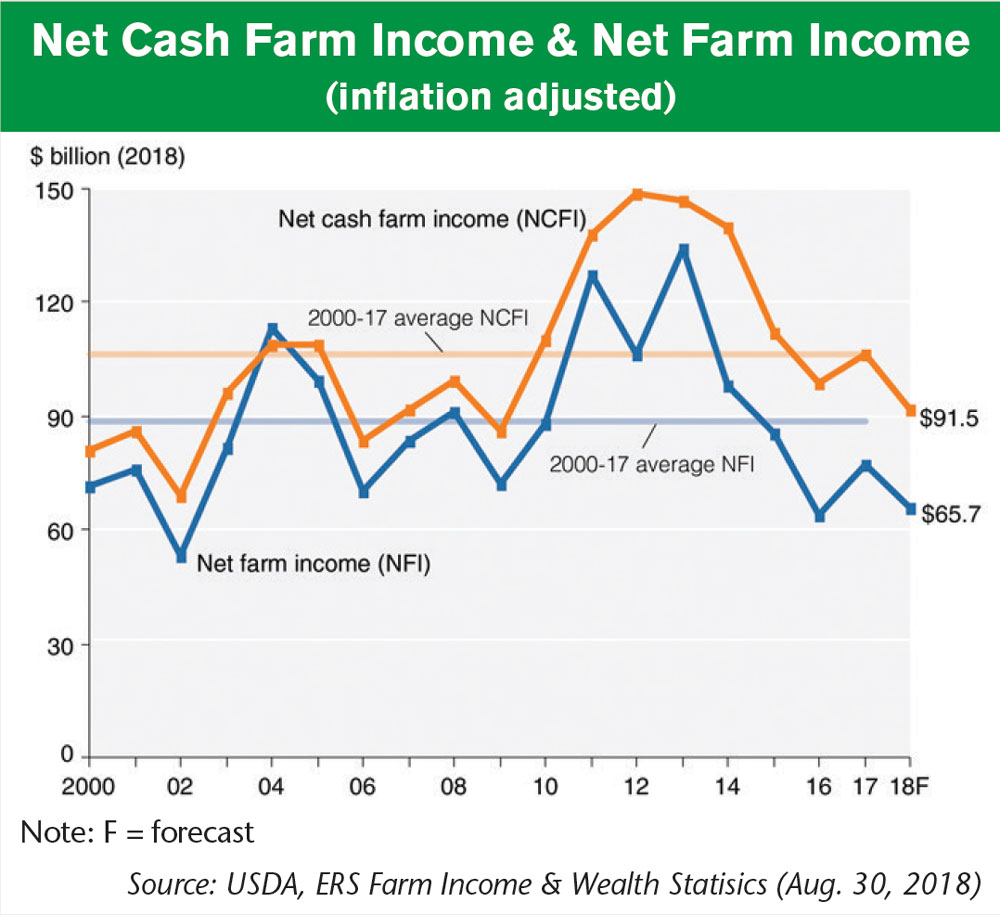

Even more so than farm cash receipts, net farm income serves as a good indicator of when farmers are able to make large capital investments, such as the purchase of new equipment.

And if the current outlook for farm profits holds true, the replacement cycle buying that has propped up North American farm equipment sales the past few months could be short lived. According to data released Aug. 30 by USDA’s Economic Research Service, inflation-adjusted U.S. net farm income is forecast to decline $11.4 billion, or by 14.8%, from 2017 to $65.7 billion in 2018, while inflation-adjusted U.S. net cash farm income is forecast to decline $14.6 billion, or by 13.8%, to $91.5 billion. According to ERS, the forecast declines are largely due to higher production expenses, which if realized, would reduce net income.

Additionally, government payments are forecast to decline $2.3 billion, or by 19.1%. However, the 2018 forecast for government payments, net farm income and net cash income do not include payments under the Market Facilitation Program (MFP) announced on Aug. 27. This program provides aid to farmers who are feeling the effects of ongoing trade tensions, including tariffs on commodities from China. It’s too early to know the impact this program will have, since it’s unclear how many farm producers will complete the MFP enrollment and receive payment in 2018.

In its recent baseline update for U.S. farm income, the University of Missouri’s Food and Agricultural Policy Research Institute (FAPRI) factors in the MFP’s first round of payments which were announced in late August. FAPRI assumes $4 billion in payments will be made in 2018 and another $700 million will be made in 2019. These payments “help push 2018 direct government payments to the highest levels since 2006,” says FAPRI.

FAPRI’s own estimates of farm income show net income falling $3.16 billion, or 4.2%, to $72.3 billion in 2018 vs. last year. FAPRI also projects net farm income to fall by another $2.8 billion (3.9%) to $69.5 billion in 2019 before rising again to near-2017 levels in 2020.

Inflation-adjusted net farm income is forecast to be just slightly above its level in 2016 and at its second lowest level since 2002, according to USDA. Inflation-adjusted net cash farm income is forecast to be at its lowest level since 2009. Net cash farm income measures cash receipts from farming as well as farm-related income, including government payments, minus cash expenses. Net farm income is a more comprehensive measure that incorporates non-cash items, including changes in inventories, economic depreciation and gross imputed rental income.

Post a comment

Report Abusive Comment